what credit cards are the best at paying you back for using them ? cabeals and scheels don’t give back much, kind of a joke

IDO » Forums » Fishing Forums » General Discussion Forum » credit cards

credit cards

-

September 28, 2018 at 7:04 pm #1800328

You’re absolutely right, the Cabela’s card is an extremely bottom-line rewards card. I got mine a long time ago because the thought of getting points was awesome. I’ve only got two, and the other is Discover. You can redeem Discover points for a lot of different gift cards, including Cabela’s/BPS, and I believe it’s actually a better rate, so I can get more Cabela’s stuff from Discover than their own CC. No annual fee on Discover, 1% cashback on purchases and a rotating 5% back on different places each quarter. I’m sure there are plenty of other great ones out there, that’s just what I use.

ClownColorInactiveThe Back 40Posts: 1955September 28, 2018 at 7:32 pm #1800334

ClownColorInactiveThe Back 40Posts: 1955September 28, 2018 at 7:32 pm #1800334Citicard double rewards always seems to get great reviews. It’s 2% cash back with no max…granted you pay it off. No of that random 5% here and there every month…just straight 2% on everything. No annual fee.

Kevin Yopp

Posts: 192September 28, 2018 at 7:58 pm #1800337

Kevin Yopp

Posts: 192September 28, 2018 at 7:58 pm #1800337If you spend much on Amazon the Amazon Prime VISA is good. 5% back on Amazon purchases and 2% at restaurants ad 1% elsewhere.

September 29, 2018 at 7:37 am #1800359American Express Primier Gold. The most versatile rewards system out yhere. 2 percent on everything, 3 percent in gas/groceries and 5 percent on air and hotel.

Rewards are in points but are easily used or converted. Reward points can be used directly om Amazon or you can cash in for gift cards to hundreds of stores like Cabelas. The can also be converted to frequent flyer points to get free tickets on any airline.

And before someone says nobody takes American Express, I use it for ever purchase and I find on average 1 or 2 places a year that don’t take it.

Grouse

September 29, 2018 at 8:40 am #1800366Check out us bank cash+ visa. You get to choose categories to get 2% and 5% cash back. Everything else is 1% cash back. No annual fee like Amex.

fishingchallenged

Posts: 314September 29, 2018 at 12:59 pm #1800391

fishingchallenged

Posts: 314September 29, 2018 at 12:59 pm #1800391Fidelity, 2% cash back on every dollar spent. No limit. Cash automatically rolls right into your account with no action required on your part. Easy, effortless and no gimmicks.

September 29, 2018 at 8:25 pm #1800414Fidelity, 2% cash back on every dollar spent. No limit. Cash automatically rolls right into your account with no action required on your part. Easy, effortless and no gimmicks.

do they accept them most everywhere?

September 29, 2018 at 10:02 pm #1800419capital one……what’s in your wallet? they give you free $100 once you charge your first $1000 purchase. after that it’s like 1% cash back maybe? I should use it all the time but I still like the debit way. I think I’m up to $300 in free cash in 3 years just for buying things I needed anyway. I tried to buy a car at the dealership with it but they said no. 300 bucks is 300 bucks and that’s a really nice fishing combo.

fishingchallenged

Posts: 314September 29, 2018 at 10:52 pm #1800420<div class=”d4p-bbt-quote-title”>fishingchallenged wrote:</div>

Fidelity, 2% cash back on every dollar spent. No limit. Cash automatically rolls right into your account with no action required on your part. Easy, effortless and no gimmicks.do they accept them most everywhere?

Everywhere that accepts Visa.

September 30, 2018 at 7:54 am #1800439Capital 1 Spark card. 1.5% on everything. No limit. No fee. Call and get a check sent to you. I let mine build up to $500 and go buy myself something.

Gitchi Gummi

Posts: 3528September 30, 2018 at 3:57 pm #1800467

Gitchi Gummi

Posts: 3528September 30, 2018 at 3:57 pm #1800467Chase sapphire and freedom, am ex delta gold and capital one venture are all good cards for rewards for those looking to get started in the rewards “game” as I call it. It’s all about getting the sign up bonuses and canceling before the annual fee hits the second year (the best cards waive the fee the first year). If you can’t pay the balance every month and end up paying interest, the rewards aren’t worth it. The credit card rewards game should only be played by people who don’t maintain a balance.

Contrary to what grouse says, after having an am ex card, I’ll never have another one after I monetize the delta rewards. Tons of places don’t accept them and it’s a PITA. All big chain stores accept them but I’ve found most that don’t accept am ex are most smaller mom/pop stores, bait shops and bars/restaurants that are not chains or within city limits.

September 30, 2018 at 7:17 pm #1800482Contrary to what grouse says, after having an am ex card, I’ll never have another one after I monetize the delta rewards. Tons of places don’t accept them and it’s a PITA.

Can I have a few examples of these “tons of places”? Because I’m hunting and fishing and traveling all over the US and Canada and I run into very, very few. And it’s not like I never have cash or other cards, so the issue matters not at all compared to what I think is one of the best rewards structures out there.

I know of a parking ramp in Minneapolis near US Bank stadium that says they don’t take AMEX, but their machine takes it just fine. The Muni Liquor in Sisseton, SD doesn’t take it, which is a huge bummer on trips to Roy Lake so I have to use (gasp) my debit card and forego the massive cash back on my 12 pack. I know of one bar in Miller SD that doesn’t take it. Oh and the parking meters in Southhampton, UK don’t take AMEX, if you can freaking believe that.

Grouse

September 30, 2018 at 8:28 pm #1800493<div class=”d4p-bbt-quote-title”>Jake wrote:</div>

Contrary to what grouse says, after having an am ex card, I’ll never have another one after I monetize the delta rewards. Tons of places don’t accept them and it’s a PITA.Can I have a few examples of these “tons of places”? Because I’m hunting and fishing and traveling all over the US and Canada and I run into very, very few. And it’s not like I never have cash or other cards, so the issue matters not at all compared to what I think is one of the best rewards structures out there.

I know of a parking ramp in Minneapolis near US Bank stadium that says they don’t take AMEX, but their machine takes it just fine. The Muni Liquor in Sisseton, SD doesn’t take it, which is a huge bummer on trips to Roy Lake so I have to use (gasp) my debit card and forego the massive cash back on my 12 pack. I know of one bar in Miller SD that doesn’t take it. Oh and the parking meters in Southhampton, UK don’t take AMEX, if you can freaking believe that.

Grouse

-quite a few of the local ma’ and pa’ type places along the Mississippi River near P4 do not take American Express.

-some Sam’s Clubs do not (one in WI that we are at didn’t, but the MN one did)

-local Lake City liquor store

American Express is pretty widely accepted, but it also “sticks it to” the businesses the most with their fee structure. I know the local bait shop accepts them, but it has to be a minimum $50 purchase. A friend who owns a local body shop said that they are just going to a flat 5% fee on any and all cards used for transactions. They’d prefer cash or check hands down and do the best work of anyone within a good hour, so it shouldn’t be an issue.

I don’t use a CC at all. My debit card probably has 5-6 transactions a month and that’s it. I’m old school and prefer cash. My wife uses hers for everything and just pays off every single cent before the end of the month. I’ll often give her chunks of cash for large purchases and she prefers to then use her card to gain the travel rewards.

September 30, 2018 at 8:46 pm #1800495American Express is pretty widely accepted, but it also “sticks it to” the businesses the most with their fee structure. I know the local bait shop accepts them, but it has to be a minimum $50 purchase. A friend who owns a local body shop said that they are just going to a flat 5% fee on any and all cards used for transactions. They’d prefer cash or check hands down and do the best work of anyone within a good hour, so it shouldn’t be an issue.

You are correct. AE is the most expensive card for fees to the business. Discover also has a high fee structure. The earn back on these cards comes out of the business owners fees. The card companies expense come in the form of bookkeeping costs.

Gitchi Gummi

Posts: 3528September 30, 2018 at 8:53 pm #1800496Grouse – pretty much any bar/restaurant type place north of Duluth in my neck of the woods and most of the bait shops. Come on up if you don’t believe me.

October 1, 2018 at 8:09 am #1800523AE Blue Cash Everyday. 3% groceries, 2% gas and some retail and 1% everything else.

Also use Chase Freedom and Discover IT which ave 5% rotating categories and 1% everything else.

Also use Chase Freedom Unlimited which has 1.5% unlimited. Would replace this card with the Citi double cash if they ever offered a incentive.

All of the above cards are no annual fee. This is free money and if you set up auto bank transfer and pay off monthly is pretty painless.

TumaInactiveFarmington, MNPosts: 1403October 1, 2018 at 8:16 am #1800525

TumaInactiveFarmington, MNPosts: 1403October 1, 2018 at 8:16 am #1800525I don’t mind my Cabelas card. I know it doesn’t have the best reward program but it is easy to use, accepted everywhere, and walking out of the store with a free auger and reel was nice. At the checkout they ask if you would like to use your points today or not. All the other rewards programs I never used because I would have to jump through hoops to get my rewards to me.

Gitchi Gummi

Posts: 3528October 1, 2018 at 10:11 am #1800554Another food for thought item… Typically speaking, the travel reward cards are more lucrative than straight cash back options. My last five vacations have been entirely paid for by credit card rewards, and I still have about 2-3 vacations worth of points to utilize on my chase and am ex cards. This is all from normal spending, just utilizing CC sign up bonuses and the referral bonuses. The best way to monetize is to play the game with your spouse.. I.e. Spouse A signs up for the card first, combine spending on one card until you hit the initial spending bonus, refer Spouse B to the same card and get the referral points. Use or transfer the points to a different card (i.e. a free one like the chase freedom). Rinse and repeat with a different card. A lot of times you can get additional points just for adding someone (i.e. your spouse) onto your CC account as an authorized user. They get their own card attached to your account, and they make 1 purchase (could be for a $2 coffee), then you get add’l 5,000 pts for the Chase sapphire for example. Then when Spouse B opens the sapphire in their name (to which you referred them which got you 10,000 add’l points), they add you to their account, you make one purchase and then Spouse B gets 5,000 extra points. Its amazing how much free money is out there is you are smart about it.

If you don’t like taking vacations every year, then cash back is probably a better option than travel rewards cards. Points can always be converted to cash back if you want to go that way. There are tons of websites out there where people are extremely serious about how to best monetize credit card rewards. Google search “travel miles 101” if you are interested.

TumaInactiveFarmington, MNPosts: 1403October 2, 2018 at 7:33 am #1800801I just received the new terms from Cabelas/bass pro Visa and now am thing of changing my card to something different.

October 3, 2018 at 9:19 pm #1801256what changed?

You still earn points. 2% on pushases at Cabelas and 2% on purchases at CENEX stations. 1% everywhere else.

Gitchi Gummi

Posts: 3528October 4, 2018 at 7:31 am #18013121% is the absolute minimum a card should offer in terms of rewards – nothing special about that at all. There are a lot better options out there.

blackbay

Posts: 699October 4, 2018 at 9:12 am #1801336

blackbay

Posts: 699October 4, 2018 at 9:12 am #1801336<div class=”d4p-bbt-quote-title”>grizzly wrote:</div>

what changed?You still earn points. 2% on pushases at Cabelas and 2% on purchases at CENEX stations. 1% everywhere else.

I’d like to know what changed also. I’ve thought about dumping my Cabela’s card also but the cards I’ve checked all have a much higher APR. I try to keep the card paid off or at least a super low balance, typically only after Christmas, so a low APR is nice to have available. I also don’t use the card much so the rewards aren’t a big factor.

I’m ticked at Cabela’s/BPS but what is the difference between me keeping their Capital One card and me getting a different Capital One card, or even a different companies card?

Rod Bent

Posts: 360TumaInactiveFarmington, MNPosts: 1403October 4, 2018 at 9:57 am #1801346They changed to MasterCard and my APR went way up. But after looking around the APR is still better than most. I was thinking about a Amazon card with 5% back at Amazon but that card has a 24.something% APR. I budget well but things come up like range, water heater, and water softener all going out in the same month.

It seems like the better the rewards the higher the APR.October 4, 2018 at 10:14 am #1801351

It seems like the better the rewards the higher the APR.October 4, 2018 at 10:14 am #1801351They changed to MasterCard and my APR went way up. But after looking around the APR is still better than most. I was thinking about a Amazon card with 5% back at Amazon but that card has a 24.something% APR. I budget well but things come up like range, water heater, and water softener all going out in the same month.

It seems like the better the rewards the higher the APR.

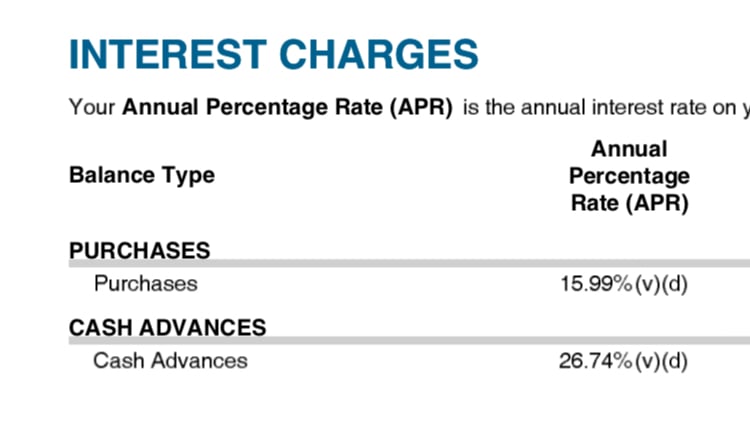

It seems like the better the rewards the higher the APR.Not sure where you’re seeing the 24% APR but mine is only 15.99% on my Amazon card. I’m sure it all depends on your credit as well.

Attachments:

A18940C1-7EB3-4967-80B6-48183CFA0F93.jpeg

ClownColorInactiveThe Back 40Posts: 1955October 4, 2018 at 10:50 am #1801363I’m sure you guys do this but one phone call every 6 mos or so and you can have that APR really low…

October 4, 2018 at 10:53 am #1801366I do like my Cabelas Visa Card. As a Black member I love the free stuff I get from my Cabelas bucks. If I ever need something for the boat or fishing, I order it using my Cabelas bucks. Same goes for BPS now… Now my wife can’t yell at me for spending money on fishing crap haha!.

I put EVERYTHING on my CC but go home and pay it off right away. Anytime we make big purchases goes on the card and we pay it off the next day. In the 10 years I have had it I have never held a balance, but I have definitely taken advantage of the cabelas bucks!

October 4, 2018 at 11:09 am #1801368Check out us bank cash+ visa. You get to choose categories to get 2% and 5% cash back. Everything else is 1% cash back. No annual fee like Amex.

I dumped my Cabelas card for this a couple years ago. I choose 2% for fuel and one of my 5% categories is Sporting Good (Cabelas). The 5% is good up to 2,000 per period I believe, which wasn’t a big deal to me. 1% on everything else.

Racked up a few thousand in rewards since I opened it.

You must be logged in to reply to this topic.