If you never file a claim and are sick of high premiums, do you carry a liability only policy?

Almost willing to try it if everyone was insured. That is another reason for the high cost. Too many uninsured drivers out there.

IDO » Forums » Fishing Forums » General Discussion Forum » Car Insurance Rate Increase

If you never file a claim and are sick of high premiums, do you carry a liability only policy?

Almost willing to try it if everyone was insured. That is another reason for the high cost. Too many uninsured drivers out there.

Looks like the problem started years ago.

Google says 9.9% to 12.5% of MN drivers are uninsured.

insurance-problem.jpg

They let you go……..

What happens when you get pulled over and don’t have insurance?

They let you go……..

<div class=”d4p-bbt-quote-title”>Rodwork wrote:</div>

What happens when you get pulled over and don’t have insurance?

A guy ran into the side of my FW’s car, obviously his fault.

She called Rochester city cops who came and agreed, it was the other guys fault 100%. Cop looks at his insurance info and it’s expired. So instead of writing him a ticket, so there’s a record of it, they let the guy go with just his license information.

We submit the claim to my insurance company and give them his expired information that turns out, they don’t have valid policy for that vehicle anymore so hey don’t acknowledge the claim. Called cop, who went to the guys house and after many calls back and forth, they said they couldn’t help us.

WTF!! You didn’t give the guy a ticket for expired insurance and know where he lives and you still can’t do anything? Like maybe arrest the guy for showing false insurance information!

My insurance covered it and said they would go after the guy which I never heard back anything.

Meanwhile, my insurance jumped 50% because she had an accident on her record!

So yeah, they do just let em go.

I was hoping something had changed. About 16 years ago I was going out of the bank when I saw a Somalian trying to park. I yelled for him to stop because I could clearly see he was going to hit my car. He stopped, looked at me, and smashed in my bumper causing damage. Not as much damage there was going to be since I got him to stop but still damaged. When the cops came they forgot how to speak English and had no insurance. Was told gambling was against their religion and insurance is a form of gambling. I said driving is a privilege and in order to enjoy that privilege you must have insurance. He gave me a what are you going to do look, let them go without a ticket, and all the damage they caused was up to me to take care of. ![]()

MN is a no fault state. All insurance claims are first made to your own insurance. An increase in fees has nothing to do with the other driver. Your own knowledge of what your insurance covers and adjusts because of is all the information you will ever need.

MN is a no fault state. All insurance claims are first made to your own insurance. An increase in fees has nothing to do with the other driver. Your own knowledge of what your insurance covers and adjusts because of is all the information you will ever need.

This is not correct. The no fault part refers to injury claims only. MN is a comparative negligence state where your damages are reduced by your percent of fault. If you get rear ended the other parties insurance should take care of the vehicle damages. If your injured you make a claim to your insurance for the initial treatment and if severe enough you would also make a bodily injury claim against the other parties insurance.

<div class=”d4p-bbt-quote-title”>Riverrat wrote:</div>

MN is a no fault state. All insurance claims are first made to your own insurance. An increase in fees has nothing to do with the other driver. Your own knowledge of what your insurance covers and adjusts because of is all the information you will ever need.This is not correct. The no fault part refers to injury claims only. MN is a comparative negligence state where your damages are reduced by your percent of fault. If you get rear ended the other parties insurance should take care of the vehicle damages. If your injured you make a claim to your insurance for the initial treatment and if severe enough you would also make a bodily injury claim against the other parties insurance.

This.

Riverrat, it’s OK if you don’t know the law/rules but don’t say if you don’t.

Yikes, there is a ton of misinformation in this thread, and I’d strongly recommend everyone meet their agent and have them explain your policy to you. As someone who recently worked for the big red company for 12 years, I’ll try and cover a few of the key points.

Rates are going up, as they always do with inflation, on homes and autos. On autos in particular it is due to both the cost to repair increasing as well as the frequency of claims.

Rates are state and company specific, so no you are not subsidizing FL hurricane damage, at least not directly. There is likely a minor impact as a derivative of the reinsurance market, but there would be no direct $ amount associated on your policy.

MN is called a No Fault state, but that is a misnomer, as we are NOT a no fault state, ONLY MN Personal Injury Protection (PIP) coverage is No Fault, so any bodily injuries you suffer go to your policy first, but no other portion of your coverage is handled that way. And if you do not have medical damages, you should go thru the at fault parties insurance if fault is not being contested.

Everyone is required to be insured in MN, including Somali’s, of whom I had a ton of clients. You should always get a picture of their DL and Insurance info, and if the insurance is expired the police should give them a ticket. If they don’t, you or your insurance company should be able to at the VERY minimum get a judgement against them, but that will require some effort on your behalf.

Bucky is correct on being a constant shopper or loyal customer, pick which one fits your personality and go with it. The cheapest rates I’ve ever seen were from people with SF for decades, and SF’s biggest discount (25%) is a 10 year accident free discount and comes with accident forgiveness. And I regularly re-wrote people who chased rate only to come back 6-12 mos later. Other people regularly save by shopping every year or two. If you use a broker and they set you up with a new company every 6-12 mos, they are likely doing you a disservice in rate or coverage as they get paid more on a new policy w/ a new company vs a renewal at the existing one.

Auto insurance there isn’t a big difference between companies, but some companies are mutual (owned by the policyholders) vs publicly traded (owned by shareholders) and that does impact how they operate.

Finally, you can opt out of auto insurance by getting a $50k surety bond (at least that’s what it was a couple years ago), sounds like many of you should look into this. However, you would be risking all of your assets for anything exceeding $50k, and will have to pay for your own defense. Good luck!

Everyone is required to be insured in MN, including Somali’s, of whom I had a ton of clients.

Sorry for spreading misinformation. It was what I was told.

<div class=”d4p-bbt-quote-title”>Huntindave wrote:</div>

The whole premise of insurance, is that the cost of a claim is shared by everyone equally.Thats why its such a croc. Why should I have to pay for Joe blows accidents, and why should Joe blow have to pay for mine

You do not have to participate in insurance. You can post a surety bond instead of “paying for Joe’s accidents”, so yes, you have a choice.

Looks like the problem started years ago.

Google says 9.9% to 12.5% of MN drivers are uninsured.

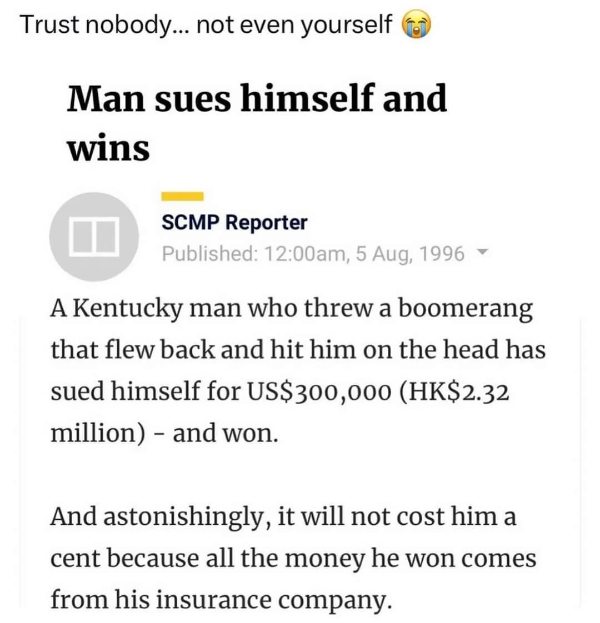

the man who sues himself and wins is not true

For the MN Libertarians

https://mn.gov/commerce/licensing/list/insurance/self-insurance.jsp

the man who sues himself and wins is not true

Even if it were true, who would be paying him? LOL

<div class=”d4p-bbt-quote-title”>Johnny wrote:</div>

the man who sues himself and wins is not trueEven if it were true, who would be paying him? LOL

In that fictional story from a satire publication it was boomerang guy’s insurance company paying him

Something else to remember if you are contemplating full coverage vs liability only. Minnesota only requires you to carry a 10k liability amount(Maybe bigwerm can explain better) which means that if someone else hits you and even if they admit fault their insurance company will only pay for damages up to 10k anything over that is up to you or your insurance to cover if you have full coverage. So say the damages are $15k their insurance pays the first $10k then if you have full coverage your insurance will pay the remaining balance minus your deductible that you pay. If you don’t have full coverage you are on the hook for the remainder. I have seen this happen and it comes as a shock since most people don’t know about it.

Last week State Farm had a press release that this year they will not be renewing 72,000 homeowner policies in California. It doesn’t surprise me that MN is following suit. My personal opinion is that they are preparing for the next round of mostly peaceful protests this next November through January.

Yikes, there is a ton of misinformation in this thread, and I’d strongly recommend everyone meet their agent and have them explain your policy to you. As someone who recently worked for the big red company for 12 years, I’ll try and cover a few of the key points.

Rates are going up, as they always do with inflation, on homes and autos. On autos in particular it is due to both the cost to repair increasing as well as the frequency of claims.

Rates are state and company specific, so no you are not subsidizing FL hurricane damage, at least not directly. There is likely a minor impact as a derivative of the reinsurance market, but there would be no direct $ amount associated on your policy.

MN is called a No Fault state, but that is a misnomer, as we are NOT a no fault state, ONLY MN Personal Injury Protection (PIP) coverage is No Fault, so any bodily injuries you suffer go to your policy first, but no other portion of your coverage is handled that way. And if you do not have medical damages, you should go thru the at fault parties insurance if fault is not being contested.

Everyone is required to be insured in MN, including Somali’s, of whom I had a ton of clients. You should always get a picture of their DL and Insurance info, and if the insurance is expired the police should give them a ticket. If they don’t, you or your insurance company should be able to at the VERY minimum get a judgement against them, but that will require some effort on your behalf.

Bucky is correct on being a constant shopper or loyal customer, pick which one fits your personality and go with it. The cheapest rates I’ve ever seen were from people with SF for decades, and SF’s biggest discount (25%) is a 10 year accident free discount and comes with accident forgiveness. And I regularly re-wrote people who chased rate only to come back 6-12 mos later. Other people regularly save by shopping every year or two. If you use a broker and they set you up with a new company every 6-12 mos, they are likely doing you a disservice in rate or coverage as they get paid more on a new policy w/ a new company vs a renewal at the existing one.

Auto insurance there isn’t a big difference between companies, but some companies are mutual (owned by the policyholders) vs publicly traded (owned by shareholders) and that does impact how they operate.

Finally, you can opt out of auto insurance by getting a $50k surety bond (at least that’s what it was a couple years ago), sounds like many of you should look into this. However, you would be risking all of your assets for anything exceeding $50k, and will have to pay for your own defense. Good luck!

Thank you for posting factual information. This will probably be helpful to someone.

Something else to remember if you are contemplating full coverage vs liability only. Minnesota only requires you to carry a 10k liability amount(Maybe bigwerm can explain better) which means that if someone else hits you and even if they admit fault their insurance company will only pay for damages up to 10k anything over that is up to you or your insurance to cover if you have full coverage. So say the damages are $15k their insurance pays the first $10k then if you have full coverage your insurance will pay the remaining balance minus your deductible that you pay. If you don’t have full coverage you are on the hook for the remainder. I have seen this happen and it comes as a shock since most people don’t know about it.

This is pretty much correct, in MN the minimum liability coverage required is 30/60/10, and people can have the liability minimum of 30/60/10 and still have full coverage. So just thinking having full coverage = good coverage, is not inherently true.

What 30/60/10 means is if someone with that coverage hits you, your medical damages are only going to be covered by the 20k PIP (aka no fault) coverage on your own policy, and 30k on the at fault parties insurance. The 60k is aggregate for the year. And the 10k is PD (property damage) coverage for repairing or replacing your vehicle, so Stanley’s example is right, and how many vehicles on the road these days are worth 10k or less if totaled out? If someone is at fault but only has 10k in coverage either your full coverage kicks in, or if you only have liability you have to sue that person in civil court. Good luck collecting, but there will be a judgement against them at least. Also, most people that I wrote that came from an online insurer (Progressive, Geico etc.) had the state minimum 30/60/10 liability coverage, as their websites emphasize price over what you are actually buying. And it’s super affordable to go to a higher and much better liability coverage. This is in addition to the roughly 10% of people driving around uninsured. Thanks for coming to my TedTalk! ![]()

![]()

crazy state farm since I was 19, now 76 rates skyrocketing, home owners up $600 this year just a couple of claims in my life. Shopped a bit, found auto homeowners $200 higher! this op homeowners. crazy bad

Both of BigWerms post were dead on. Far to many people just don’t understand the basic concept of insurance, let alone the Various coverages of their own personal policy. I have said it several times on these insurance post, Make a appointment with your current agent and take a hour or so of your time discussing your policies with them. Have them explain each of the coverages to you. The coverages on auto insurances are basically the same but can really be different when it comes to home policies. Far to many people opt for the State Minimum coverage on their auto policies. This is all well and fine if you nor anyone driving your car has a accident that they are ruled at fault for. 10,000 of property damage is not going to cover many of the cars that are on the road these days. The insurance company will write a check for up to the 10,000 of coverage you have and their obligation is met. The person with the 50,000 totaled auto is not going to just accept that and move on. The other party or their insurance company is going to file a lawsuit against you and you are going to end up losing and owing. It’s even worse if the person is injured badly. Once again your insurance company is going to pay up to the 30,000 limit and their obligation is met. If their injuries exceed that 30,000 ( Not real hard these days ) once again you are going to end up in a lawsuit and lose. Its more than just the injuries that come into play. Its also lost wages from work, Pain and suffering, Ect. Its just not worth the risk for a few $’s of savings a month.

Two other things that most companies offer to help lower your auto insurance cost are:

Near a 10% discount if you are over 55 years of age and take a 55+ defensive drivers class. These can be either taken in a classroom or online. They are good for 3 years. That adds up to a decent amount of savings over 3 years.

Some type of device that tracks your driving habits. This can usually save you a addition 5-10%.

Be sure to ask your agent about these discounts when you sit down with them to review your policies.

Insurance companies are no different than other companies, They are not in business to lose money. Sadly many/most have lost money in the last few years here in Minnesota. Minnesota is one of the highest claim cost states in the nation. Thus they are one of the highest premium cost in the nation. Minnesota has been once of the highest hail claim states for several years now. They are also one of the highest animal collision claim states each year. Insurance companies are also Regulated by the state government. All rate increases must be approved by them. They also control how much funds insurance companies have to have available in case of large losses. If those funds get depleted due to large loss events, they require they are built back up. This is one reason insurance rates have increase over the last several years.

I carry a very high liability limit (pretty sure MN max) and high under-insured and uninsured limits by choice. Price is high but I am not going to be underinsured. Zero tickets and zero accidents with any fault on anyone in the policy …

The cost of that insurance on our third vehicle driven by our young adult child is insanely high. He pays for part of the insurance that would be “normal”. I thought about selling him the car having him lower the limits to a more reasonable level.

If you are rear ended … the other vehicle is at fault… nothing goes through your own policy unless you choose to or the other driver has insurance issues.

A decade or more ago my mom’s car was parked at night and rear ended in a small town. It was totaled and the claim was originally on her policy. Since there was no other driver identified she was on the hook for the deductible.

Turns out it was hit by bubba around 1:30AM obviously coming home drunk. Ironically the same guy was in a demolish’n derby that next weekend at the county fair.

OK – small town and we get the name. Nothing happens and my mom’s insurance agent says they are not getting any accident reports from the local sheriff.

I call the sheriff and he has the gall to say “your mom was insured so we didn’t file the report” … I say yep, but she is on the hook for the deductible. I tell him my next call is to the State Highway Patrol who has agreed to investigate if I call back (true). Sheriff says report will be filed by end of day … my mom got her money.

On home owners … make sure you are actually covered on your sporting goods equipment (especially guns) and build in riders to cover gaps or live with the policy as is knowing the potential for loss.

One thing with insurance is never assume!

If you are rear ended … the other vehicle is at fault… nothing goes through your own policy unless you choose to or the other driver has insurance issues

If you are the non at Fault party in a accident and the other party has insurance I would always process the claim through the other parties insurance if possible. If you start down that road and run into a issue, you can always open the claim with your insurance company if needed. If you open the claim at your own insurance company your deductible will most likely come into play until your insurance company is able to recover the money from the other parties insurance company. This is assuming the other party assumes responsibility for fault of the accident or the police assign fault to the other party.

Whenever possible when in a accident, have law enforcement respond to the accident and make a report. If you feel like you are the non at fault party, push the officer to make sure they note in their report who they believe was the at fault party. Without some sort of proof of a at fault party, it often becomes a he said, she said, kind of thing. In these cases it often ends up that each party involved ends up picking up the cost of their insureds damages. Then you end up with a accident on your insurance record and this is not a good thing. I would push hard to have a at fault party determined by the officer right at the time of the accident.

You must be logged in to reply to this topic.