Ok. I believe you. Thanks.

IDO » Forums » Fishing Forums » General Discussion Forum » Auto insurance are we getting hosed?

Auto insurance are we getting hosed?

-

Riverrat

Posts: 1888November 26, 2024 at 11:03 am #2301535

Riverrat

Posts: 1888November 26, 2024 at 11:03 am #2301535There is no such thing as “local” insurance. North Star is the only local game in town I know of. I would never use an agent again for auto. Straight to the teet when it comes to that. Any major company will send someone to you and file a claim without an agent involved anyways. Homeowners is a different story. I don’t know if it makes a difference when filing a claim but it makes me feel better. The difference between my Progressive direct, and a local agent was that I have to pay every 6 months for direct, and I could pay yearly with an agent and pay an extra 24$ a year.

CaptainMusky

Posts: 25123November 26, 2024 at 11:10 am #2301538

CaptainMusky

Posts: 25123November 26, 2024 at 11:10 am #2301538Since I’m off all week I am going to be working on researching this more but I’m confident I’m grossly overpaying. I was doing this all from my phone so it was hard to read. I will get a quote for all vehicles maybe those won’t be much cheaper. The one car we aren’t even driving now

November 26, 2024 at 1:03 pm #2301569How do you explain the specific example I got with Progressive where my son went to the website and I went through my agent and quoted me something significantly higher for exact same coverage? The ONLY difference is one was through an agent.

I’d have to see both quotes to tell. My guess is something was different in the coverages or one picked up something different on the rated drivers than the other. Also some agents give the quote #’s before what’s called validating the policy and other only give the quote after that’s done. Its during the validating process that MVR’s and other research is done. Often the validating picks up something that raises the rates that was not on the original quote. I always push the quote thru the validation process prior to quoting a price. Also progressive is a lot different in that sometimes you can purchase direct thru the company without going thru a agent. Not sure if the premium is different direct or with a agent or not.

Brittman

Posts: 2252November 26, 2024 at 1:14 pm #2301570Two of the hailed-out roofs on our house occurred in catastrophic hailstorms that hit the neighborhood. Over 90% of the roofs in a fairly wide swath were replaced after the last storm. Well unless you had SF. I did not need a contractor on the roof with the adjuster on that one. The contractors that I spoke to all mentioned the same insurance company as difficult to work with.

Brittman

Posts: 2252November 26, 2024 at 1:23 pm #2301573No tickets, no accidents on anyone’s record and the premiums are quite large. I just looked at my renewal (end of month) and it went down 8%.

I carry the Minnesota maximum on liability (well it was the upper limit, not positive it still is). It certainly costs more especially when you have a son on your policy. I often think it would be cheaper to sell him the car and let him have his own policy. Right now, he only pays the base part of the plan and I pay the added premium for the higher liability.

I also carry the high side on both the uninsured and underinsured riders but often question if insurance companies actually pay off on those riders (and I hope that I NEVER find out). I find it difficult to have to pay for those who don’t in insurance too.

jeff becker

Posts: 43November 26, 2024 at 1:29 pm #2301574

jeff becker

Posts: 43November 26, 2024 at 1:29 pm #2301574I just bought a 2025 Ram limited. My insurance is $920 per year. I had a 2020 Ram Laramie eco diesel. The new truck premium went up $40 per year. I go through a small insurance agency. He checks new insurance companies every year to keep our rates low. We have been with the same insurance company for the last 8 years.

November 26, 2024 at 1:43 pm #2301578<div class=”d4p-bbt-quote-title”>Brittman wrote:</div>

State Farm (auto ins.) is great to work with when their customer is at fault. I will share that homes in our area with State Farm are the least likely to have roof replacements due to hail.If you want to find out what insurance companies fight people the hardest on home claims, Just ask several home contractors. The contractors I know all give me the same 2-3 companies who they have the most issues with.

If there is an actual loss, take them to Appraisal. You will win 99.9 percent of the time.

BTW – Insurance companies do not want you to know that.CaptainMusky

Posts: 25123November 26, 2024 at 2:02 pm #2301580I just bought a 2025 Ram limited. My insurance is $920 per year. I had a 2020 Ram Laramie eco diesel. The new truck premium went up $40 per year. I go through a small insurance agency. He checks new insurance companies every year to keep our rates low. We have been with the same insurance company for the last 8 years.

That’s a pretty impressive I’d say.

November 26, 2024 at 2:45 pm #2301591I can’t address all the info here at once, but I’ll try and touch on a few key points. First, Captain there is no way there were the same inputs on those two quotes. If they were identical inputs, there wouldn’t be an agent selling progressive as everyone would go online for 66% discount. If I were to guess the online one was not underwritten (credit/driving record check), Prog is notorious for this bait and switch rating and is one of the reason they lose 50% of their clients per year.

In general Auto insurance is similar across the industry, just make sure you have sufficient liability coverages and know your deductibles. The online companies (Prof, Geico etc) advertise low or state min liability coverage often and it should not even be legal imo. Like FT said not too many vehicles less than 10k out there these days, so they are setup to not cover a total loss.

Insurance operates as a margin business, previously SF (where I worked for 12 years) operated like this, for every $1 in premium they got paid, they would pay out $1.02 in claims and pay their bills with the .03-.08 investment return they cleared that year (5%-10% return on your $1 premium). They are also a Mutual company so they don’t payout stockholders and their CEO has relatively modest pay for the industry and their business size. For the last few years that model has been blown up for insurance companies with 2023 being the worst with $1.43 paid out on $1 of premium. This is due to frequency and cost of claim increasing. On average a roof used to be 20k or less, now it’s north of 40k. A windshield used to be $500 and no calibration needed, now it’s $1500+ with most needing calibration (increase in labor and equipment costs). These are two of the most common examples, but the supply chain (remember vehicle chip cost/availability?!?) and inflation issues post-Covid are impacting all areas of insurance claims.

Fwiw I now work in commercial insurance, and still have my personal with SF. And there’s a few companies I would never switch to, and I’d be happy to share via PM if anyone wants to know my personal opinion. And also don’t believe everything you read on the internet.

CaptainMusky

Posts: 25123November 26, 2024 at 2:56 pm #2301595

CaptainMusky

Posts: 25123November 26, 2024 at 2:56 pm #2301595Bigwerm thanks for the info. It did request SSN when I was doing the quote but didn’t require it so I didn’t put it in. So perhaps my rate changes after that but everything else I entered was the same and in the example I gave for my son’s results and mine the same.

November 26, 2024 at 3:03 pm #2301598If there is an actual loss, take them to Appraisal. You will win 99.9 percent of the time.

BTW – Insurance companies do not want you to know that.I don’t mind them knowing that. If fact if a customer thinks the adjusters findings were wrong I often tell them to. You are correct id there is a actual loss they will win. The key is a actual verifiable loss. Many contractors believe there is a loss when there is not.

November 26, 2024 at 6:10 pm #2301635<div class=”d4p-bbt-quote-title”>Eelpoutguy wrote:</div>

If there is an actual loss, take them to Appraisal. You will win 99.9 percent of the time.

BTW – Insurance companies do not want you to know that.I don’t mind them knowing that. If fact if a customer thinks the adjusters findings were wrong I often tell them to. You are correct id there is a actual loss they will win. The key is a actual verifiable loss. Many contractors believe there is a loss when there is not.

Oh, I agree and the Homeowner would have skin in the game at that moment.

The bad thing in MN is that the Insurance companies have very strong lobbiest’s and as a contractor I am unable to speak with the Adjuster.November 26, 2024 at 9:32 pm #2301664<div class=”d4p-bbt-quote-title”>fishthumper wrote:</div>

I can tell you that a Agent has no control over premiums or their commission rates at all. Sure wish they did. A agent doesn’t like it when rates go up any more than you do. As far as commissions goes, most agents commissions have gone down in the last 5 or so years.FT I believe you and I appreciate you commenting since you are in the field and was hoping you would reply.

How do you explain the specific example I got with Progressive where my son went to the website and I went through my agent and quoted me something significantly higher for exact same coverage? The ONLY difference is one was through an agent.I can tell you that Progressive Direct (website or phone call to Progressive) charges less to the customer than going through an independent agent. Why do you think that is? No commission paid out to an independent agent. I can also tell you that your likelihood of having poor coverage and claims service is much greater going through Porgressive Direct than through and independent agent.

November 27, 2024 at 4:04 pm #2301805as a contractor I am unable to speak with the Adjuster

I always tell my customers if possible make sure their contactor can be there at the time the adjuster will be there. The few local adjusters I know have no problem discussing the claim with the adjuster at the site. In fact most prefer it.

November 27, 2024 at 4:32 pm #2301810<div class=”d4p-bbt-quote-title”>Eelpoutguy wrote:</div>

as a contractor I am unable to speak with the AdjusterI always tell my customers if possible make sure their contactor can be there at the time the adjuster will be there. The few local adjusters I know have no problem discussing the claim with the adjuster at the site. In fact most prefer it.

I should clarify, a contractor is unable to talk policy with an Adjuster in MN. They can discuss damage and quantities.

November 27, 2024 at 4:53 pm #2301813Canopy Group

Saved a bunch of money when I switched to them. After 5 years with them and the same insurance company, they shopped around before renewal and I switched to another company and saved over $800.November 27, 2024 at 5:39 pm #2301823I just left State Farm and I’m now paying $700 less per year for all lines combined thru and fam. However, we go through this same cycle every 3-4 years. Might go back one day might not, after about 3 years I start shopping, loosely. Hand out my coverage and ask for a quote to match the exact same coverage. Whichever one comes back the cheapest is the answer.

Just my 2 cents. State Farm has been jacking rates every 6 months the past 2 years to the point that it’s outrageous for me now. Plus no discount for pay in full? Wack.

This is my first time with am fam. I went from a mutual (forget the name it was a long time ago) to state farm, farmers, state farm, now am fam. The circle of life.

CaptainMusky

Posts: 25123November 28, 2024 at 7:38 am #2301906I can also tell you that your likelihood of having poor coverage and claims service is much greater going through Porgressive Direct than through and independent agent.

I guess that is a risk I am willing to take. The only time I have contacted my agent is to add or drop a vehicle in over 15 years. Nothing like collecting a fat paycheck for basically doing nothing.

Reef W

Posts: 3210November 28, 2024 at 8:09 am #2301918

Reef W

Posts: 3210November 28, 2024 at 8:09 am #2301918I guess that is a risk I am willing to take. The only time I have contacted my agent is to add or drop a vehicle in over 15 years. Nothing like collecting a fat paycheck for basically doing nothing.

And you don’t even have to talk to an agent to do that if you don’t want, takes a few minutes on website. I also don’t understand people complaining about coverage or the minimums, it’s whatever you pick so you can match any other policy.

Every time I have talked to an agent though they’ve been really helpful. I had a lot of questions about Umbrella policy and they spent quite a bit of time going over everything with me. Another example is I called them about something (can’t remember what) but something I said made them realize we were married now. They asked date, retroactively changed previous auto policies, and refunded us for some discount we should have been getting.

CaptainMusky

Posts: 25123November 28, 2024 at 8:26 am #2301926I had a lot of questions about Umbrella policy and they spent quite a bit of time going over everything with me.

I checked into getting an umbrella policy and because I was all set in doing in they sent out some person to walk around my house without my knowledge and proceeding to identify a bunch of things about my property that were “issues” and then consequently DROPPED my effing insurance at the end of the month. Mind you if your mortgage company finds out you dont have insurance they will call the mortgage due at that point so needless to say I was pissed and scared AF and scrambled to get a new insurance company for the house. I talked to my agent about this and told him I was pissed off and he said she should have never done that without your knowledge and said they have had complaints about her before. Nothing she cited was an actual problem OR what she even said it was. She said the trim on my shed was rotting. No, I didnt sand it real well before I painted it about 10 years ago and the paint was coming off in spots. Far from rotting, not even close. She was also writing me up because I like to recycle cans and have multiple garbage cans under my deck to store them in until I bring them in.

November 28, 2024 at 9:20 am #2301933Just going through this. Have been with Progressive for my 2015 2500HD and 2022 Kia Sorento PHEV and 2013 Triton for 3 years direct and 6 years total(Kia added 2023). Originally agent gave me the best quote. Three years ago I checked Progressive direct and they were better. Last three years vehicles have gone from $600-$810-$902. Boat $318-$357-$389. I asked agent to check around. They came back with Progressive, vehicles $751 and boat $318 with $10K more replacement value. She used my Progressive direct quote figures. Pays to check.

Reef W

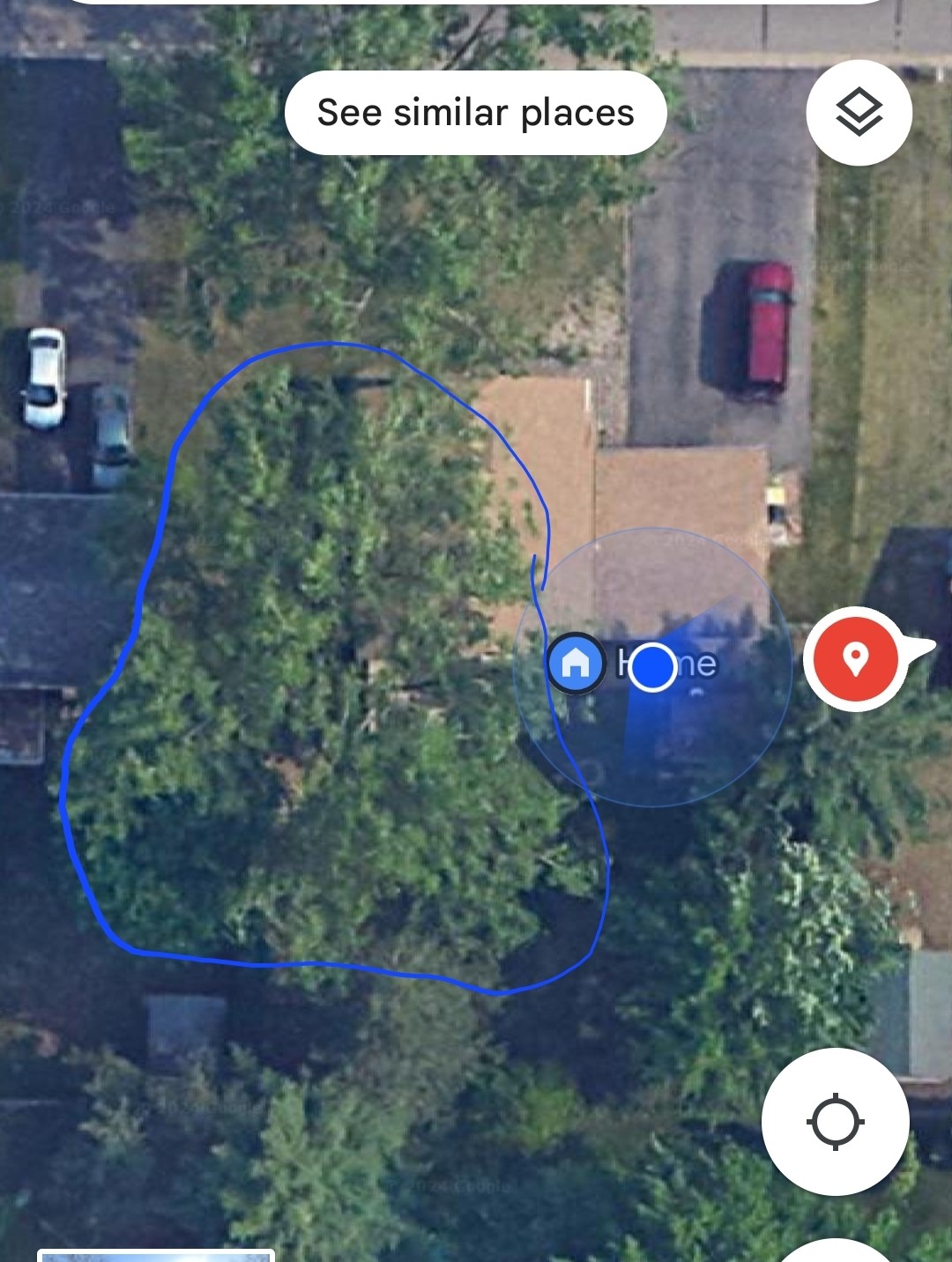

Posts: 3210November 28, 2024 at 9:21 am #2301935I didn’t get an inspection for umbrella. Changing my home insurance is an issue though because after I try to switch everyone comes and looks and says they won’t renew unless I cut down a tree that’s bigger than my house and I don’t want to so I’ve been stuck with old one that’s getting kind of expensive.

Attachments:

Screenshot_20241128_091659_Maps.jpg

CaptainMusky

Posts: 25123November 28, 2024 at 9:25 am #2301938Reef I can see why they would want that tree gone and I can understand why you wouldnt want to cut it down, but that is a dang risk for sure. WOuld suck to lose a tree like that for sure.

dirtywater

Posts: 1805December 13, 2024 at 11:39 am #2304744Time to start shopping here as well. Homeowners policy is up 42% in 2 years. Never a claim in 18 years but they’ll bend me over like anyone else. Have the house, umbrella, 3 vehicles and the boat with State Farm. Makes my head spin thinking of comparing rates on all this crap.

Snake ii’s

Posts: 560December 13, 2024 at 11:45 am #2304747

Snake ii’s

Posts: 560December 13, 2024 at 11:45 am #2304747Avoid State farm and Progressive.

Had both for years with great driving record. One moving violation (speeding) in 35+ years.

State Farm was 40% higher than Progressive so I switched. SF came back with “we can save you $$” BS – I replied why did it take me leaving to get a discount?

Progressive was reasonable for first year then started jacking the rate back up to where SF was. When I inquired why – “due to your credit score”. My credit score was in the high 700’s.

Dropped Progressive for the lizard team. Very happy with their rates.

CaptainMusky

Posts: 25123December 13, 2024 at 11:57 am #2304749Avoid State farm and Progressive.

Had both for years with great driving record. One moving violation (speeding) in 35+ years.

State Farm was 40% higher than Progressive so I switched. SF came back with “we can save you $$” BS – I replied why did it take me leaving to get a discount?

Progressive was reasonable for first year then started jacking the rate back up to where SF was. When I inquired why – “due to your credit score”. My credit score was in the high 700’s.

Dropped Progressive for the lizard team. Very happy with their rates.

Have you noticed big jumps in rates with progressive? That’s what I’ve heard here and elsewhere.

Riverrat

Posts: 1888December 13, 2024 at 1:20 pm #2304776Every time I had a big jump (45$) with progressive I just hopped online and used the chat bot to complain, a minute later a person comes on and says they rechecked my driving record and credit score and my price is going up 7-12$ for the year. This has been for the last 5 years. For the 3 years before that I had progressive still but it wasnt Progressive direct it was just progressive but still no agent. That was more variable but never more than 20$ for a year even with vehicle changes.

CaptainMusky

Posts: 25123December 13, 2024 at 1:29 pm #2304780$20 “jump” in a year? That’s peanuts. I lose that in pulltabs pretty easy.

Brad Dimond

Posts: 1603December 13, 2024 at 1:39 pm #2304782

Brad Dimond

Posts: 1603December 13, 2024 at 1:39 pm #2304782If you qualify, can’t say enough good things about USAA. Going through an auto claim now and they’ve made it as simple as could be. Online claim filing, picture upload and follow up with an adjuster was painless. Scheduled within 4 days for an estimate and can leave the vehicle with the shop doing the estimate for the repairs. Rental car will be dropped off at the body shop while I am there, will be picked up from the body shop when I get my vehicle back. Rates are better than State Farm (our previous insurer) and service is great.

You must be logged in to reply to this topic.